Background

The role of a pension scheme trustee is never an easy one, but 2022 proved to be an extraordinary year with many pension funds facing significant challenges on their investment strategies.

Those managing “Defined Benefit” pension schemes often use a strategy known as Liability Driven Investment (or “LDI”). In summary, this involves the use of leverage to amplify returns to meet the obligation to pay pension fund members. This strategy will be more attractive where borrowing costs or the cost of the leverage is low, and therefore has worked well over recent years. However, the extreme market volatility in the Autumn of 2022 has called into question the efficacy of this approach and exposed some opaque risks. There are now questions being asked of pension fund advisors, managers and trustees. More fundamentally, have pension scheme members suffered detriment? This note seeks to explore this strategy and considers where disputes may arise in the pension management industry.

What is LDI?

LDI is a risk management strategy which aims to mitigate the interest rate and inflation risks related to a pension scheme’s future liabilities (i.e., the obligation to pay pensions in the future) by building a portfolio of assets with a similar income profile to the future payments due. In short, the strategy seeks to recreate an asset portfolio with a return that mirrors the expected payments the pension fund is going to need to make.

Where the assets of a scheme are insufficient to meet the future requirements, i.e., the fund is in deficit, the scheme manager may look to increase returns by introducing leverage into the LDI portfolio. This happens through borrowing either to invest in a greater value of lower risk assets (like gilts) or to free up resources to invest in assets that may yield higher returns.

Introducing leverage amplifies the returns on the portfolio of assets, but also amplifies the losses if the investments decline. By the end of 2022, 60% of trustees were using some form of LDI strategy. In the UK, the pension industry is regulated by The Pension Regulator (TPR) and LDI strategies must be accessed through specialist funds which should have strong risk governance to monitor the risks being taken. Pension scheme trustees must take professional advice (from investment consultants, fund managers and regulators) as to whether the strategy is appropriate before entering an LDI approach.

The Risk of Leverage

The leverage in LDI allows schemes to retain some of their assets in growth seeking assets (e.g., equites, corporate bonds, private markets) the return on which should reduce the pension deficit (any shortfall in assets to meet liabilities) in the longer term.

In an LDI strategy, the fund will borrow from either banks or market sources and use the borrowed funds to finance the LDI strategy. This borrowing will typically require a margin to be posted by the borrower at the outset of the loan as security, usually in the form of cash or gilts, and will need to be topped up if the value of the investments selected falls. Ordinarily, as high-quality government bonds are not volatile instruments, the payment or return of this margin would be an operations function of limited interest to the market. However, this changed abruptly in September 2022.

Market Volatility

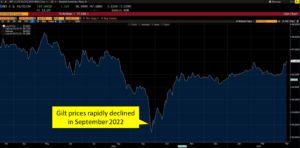

In reaction to Kwasi Kwarteng’s mini budget on 23 September 2022, the price of gilts collapsed as investors required a higher interest rate to compensate for the perceived deterioration in UK credit worthiness. The rapid decline in the price of gilts resulted in the lenders demanding margin payments to cover the mark-to-market losses. Many LDI schemes were invested in gilts and posted these as margin collateral to their lenders. The margin calls exceeded available cash, requiring pension fund managers to sell gilts to raise cash. This placed even further downward pressure on gilt prices. This created a vicious cycle as further selling pressure on the gilt market caused prices to decline, and further margin to be needed.

UK Treasury 0.125% Gilt for 31 January 2024 Daily Last Price from 15 March 2022 to 15 March 2023, extracted from Bloomberg.

A perfect storm of an absence of buyers, multiple LDI fund sellers and the shattering of confidence in the UK led to an unprecedented decline in gilts (and rise in interest rates) as illustrated by the chart of the UK Treasury 0.125% Gilt for 31 January 2024 above. Soon after, the Bank of England stepped in as a ‘buyer of last resort’ to remedy the market chaos. The market recovered over the remainder of 2022.

What now?

The magnitude and speed of the move lower in gilt prices has shocked the industry. Pension schemes were forced sellers of gilts at distressed prices and at some level this has diminished their ability to meet future pension liabilities. In the aftermath, there is now increased scrutiny on LDI strategies and the pension industry from politicians, regulators, and the media. The questions that will need to be addressed over the coming months include:

•Have pensioners been harmed and if so, what detriment have they suffered?

•Does pension regulation need to be enhanced (with a focus on the allowable leverage in LDI or enhanced liquidity requirements)?

•Did pension fund managers breach their investment management agreements with their LDI strategy?

•Were the governance arrangements put in place by pension trustees adequate?

•Was the advice provided by investment consultants appropriate?

Parliamentary enquiries are underway and regulators and central banks are calling for measures to develop greater resilience. Earlier this month, Sir Nigel Wilson, the Chief Executive Officer of Legal and General, the largest provider of LDI products, announced a £225 billion drop in the value of assets managed by its fund management arm (a decline of 16%). He asserted that the events in September 2002 were unpredictable and due to the lack of co-ordination between the Kwasi Kwarteng mini budget and the Bank of England’s plan to begin quantitative tightening with the selling of gilts.

In our view, the inquest into the scale of the damage and who (if anyone) is to blame or suffered detriment has only just begun. Whilst this topic has now moved from the front page, it will occupy the business pages for the foreseeable future and may well lead to a variety of disputes as answers emerge to the questions posed above.